Market Structure & Digital Money

08: The global banking pivot: why tokenised deposits and compliant stablecoins are the emerging mainstream

Major banks are testing stablecoins and tokenised deposits. Here is what that trend means for the UK regulatory direction, settlement infrastructure, and the future of onchain finance.

Newsletter

Get New Research In Your Inbox

When we publish a new article, you will be the first to know.

Banks and stablecoins: why the mainstream is moving toward regulated tokenised money

The financial industry is undergoing a profound transformation as technology, regulation, and investor expectations continue to evolve. At Liquida, we closely follow these developments while building solutions designed to address some of the most persistent inefficiencies in modern financial markets.

Our team is focused on understanding where the industry is heading and how emerging platforms, technologies, and investment models will shape the next decade of financial infrastructure. You can learn more about our mission and the team behind the project on our About Us page.

The shift is already happening

The conversation around digital money is often framed as a competition between models, stablecoins versus bank deposits. Private money versus public money. New infrastructure versus legacy systems.

In practice, the direction of travel is more nuanced, large financial institutions are not selecting a single approach. They are simultaneously exploring multiple forms of tokenised money, each aligned to different use cases, regulatory constraints, and settlement requirements. This is increasingly visible in the activity of major banks globally, as well as in the UK’s policy direction.

What the large-bank stablecoin consortium is actually doing

Recent reporting indicates that a consortium of major banks including Bank of America, Deutsche Bank, Goldman Sachs, UBS, Citigroup, Mitsubishi UFJ Financial Group, Toronto-Dominion Bank and BNP Paribas are actively exploring stablecoins linked to G7 currencies. This activity is not being driven by speculative demand, rather, it reflects a recognition that:

- programmable settlement is becoming necessary

- cross-border payment infrastructure is evolving

- digital asset markets require compatible money layers

Crucially, these efforts are framed explicitly within regulatory boundaries, emphasising compliance, risk management, and integration with existing systems.

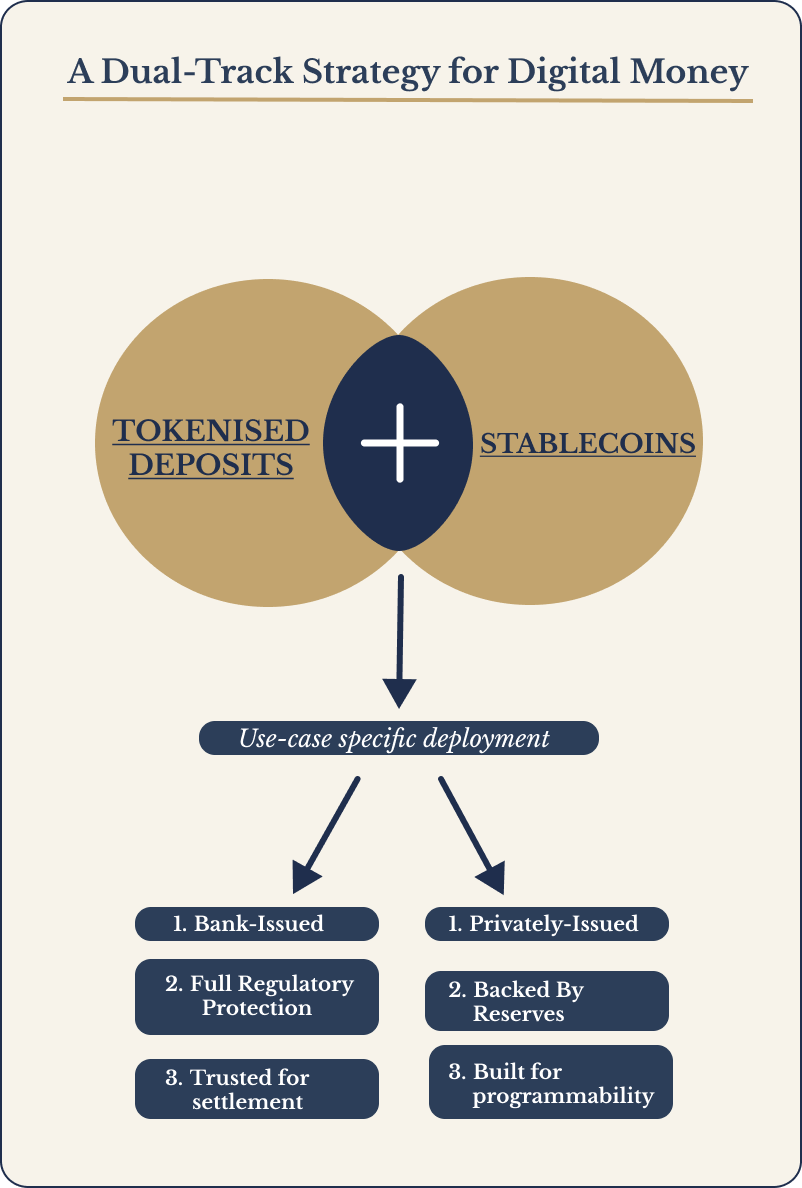

The emerging bank strategy: dual-track money

The UK angle: tokenised deposits as the foundation layer

In the UK, the development of tokenised money is not limited to stablecoins. The GBTD (Great British Tokenised Deposits) initiative, coordinated by UK Finance, provides a clear example of how banks are approaching the problem. The project positions tokenised deposits as:

- extensions of existing bank money

- fully within the regulatory perimeter

- aligned with current protections

This reflects a deliberate design choice, rather than introducing entirely new forms of money, tokenised deposits aim to modernise existing monetary infrastructure, making it interoperable with digital systems while preserving trust.

Stablecoin testing in regulated conditions

At the same time, stablecoins are being explored in controlled environments, examples of UK testing initiatives indicate that stablecoins are being trialled for:

- payments

- wholesale settlement

- interaction with digital asset platforms

Importantly, these tests are occurring within:

- regulatory sandboxes

- defined supervisory frameworks

- explicit compliance constraints

This aligns with the broader UK approach of innovation within the perimeter, not outside it.

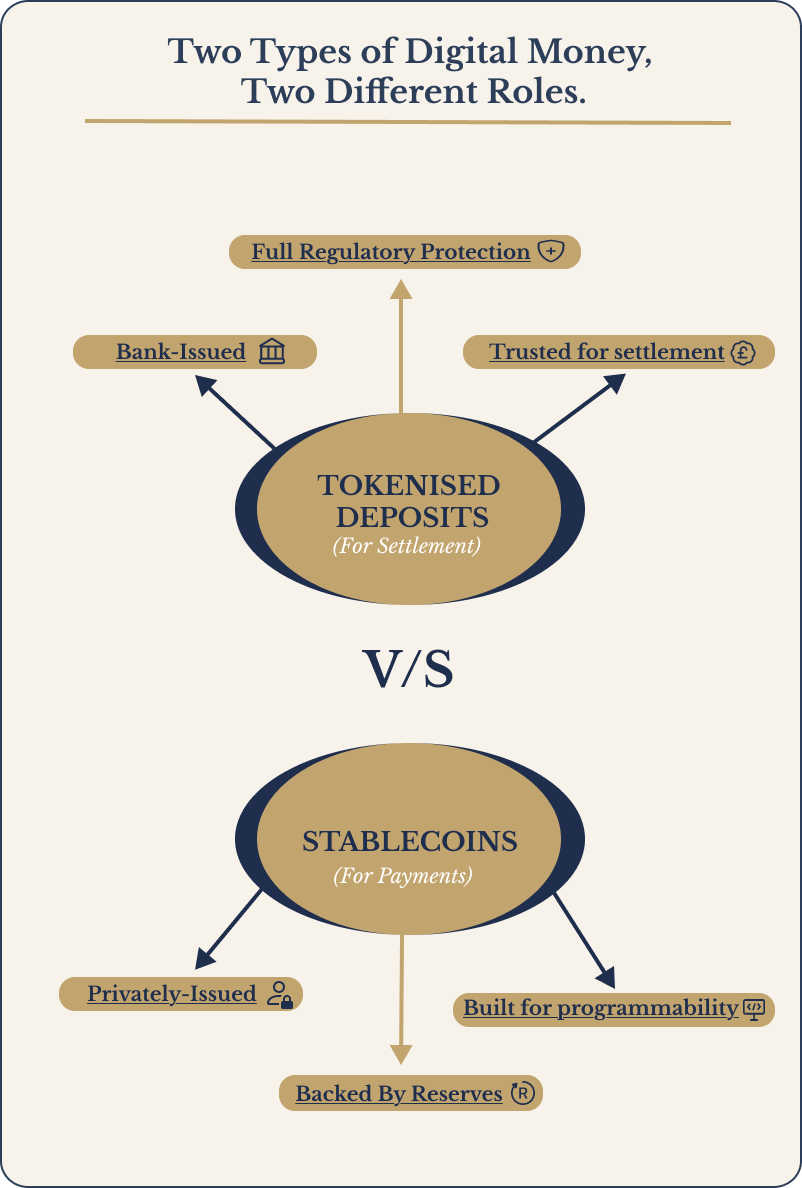

Functional Roles of Tokenised deposits vs stablecoins

What this implies for RWAs

Across these developments, a consistent pattern is beginning to emerge, rather than converging on a single form of digital money or infrastructure, markets appear to be evolving toward a model defined by the interaction of three components: programmable assets, programmable settlement mechanisms, and a regulated money layer.

This framework is particularly relevant in the context of real-world assets (RWAs). Tokenised securities - whether in the form of funds, bonds, or other instruments - do not operate effectively in isolation. Their viability depends on a set of supporting conditions, including reliable settlement processes, access to compatible forms of digital money, and a sufficiently clear regulatory environment.

In this context, the parallel development of tokenised deposits and regulated stablecoins is significant. Together, they begin to provide the monetary layer required to support these systems, enabling tokenised assets to move beyond static representations and participate in more integrated, settlement-aware market structures.

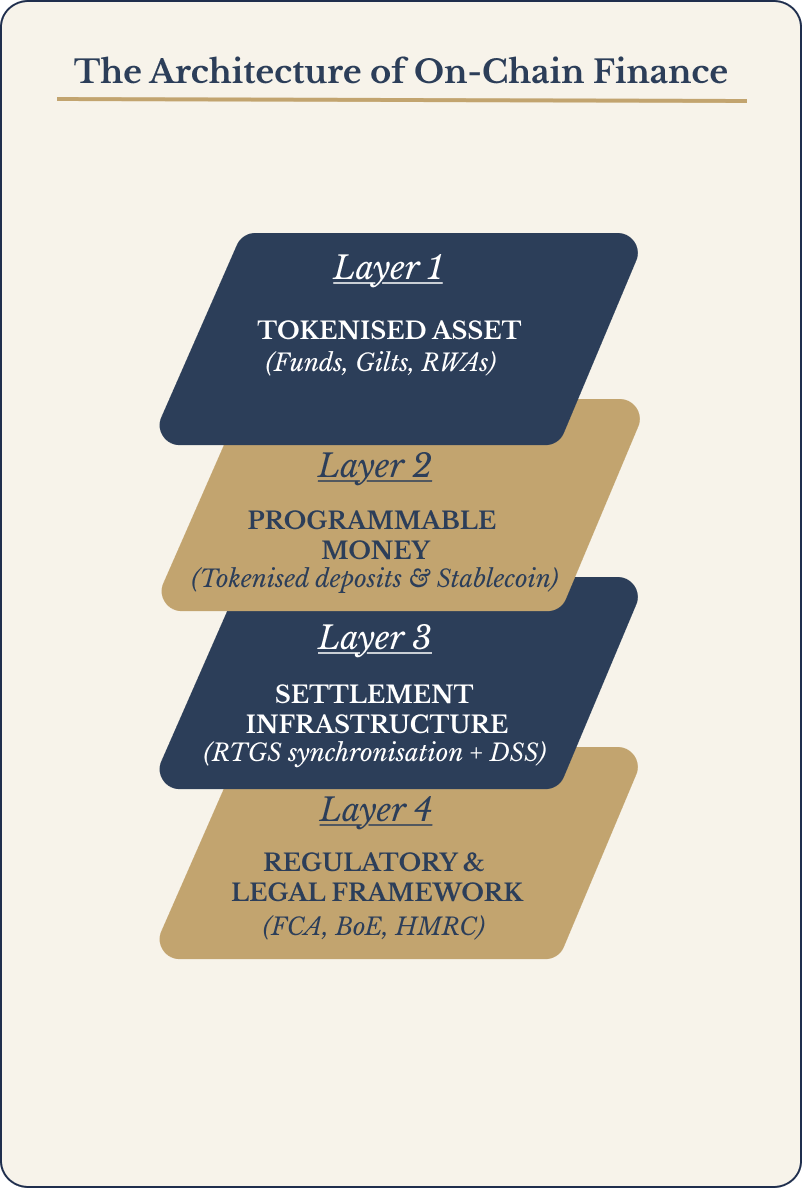

The full stack: regulated on-chain finance

We believe that the next wave of financial innovation will come from companies that combine deep market understanding with scalable technology. Our team is actively working toward building a platform designed to unlock new opportunities within the financial ecosystem.

For those interested in the people and ideas behind this initiative, you can explore the background of our team on our Meet the Team page.

FAQ

Why would banks prefer tokenised deposits?

Because they retain the characteristics of traditional bank money, including regulatory protections and integration with existing systems.

What makes regulated stablecoins different?

They are designed to operate as payment instruments, with strict requirements around backing assets, redemption, and operational resilience.

What is the role of the DSS?

The Digital Securities Sandbox provides a controlled environment where these components - assets, money, and settlement - can be tested together.

The real takeaway

The global banking system is not moving toward a single form of digital money, It is converging on a multi-layered model, where different instruments serve different functions within a unified system. Tokenised deposits provide continuity and trust, stablecoins provide flexibility and programmability. Settlement infrastructure connects both into a coherent framework. The result is not a replacement of financial infrastructure, but its gradual evolution into something more interoperable, more programmable, and ultimately more scalable.

If you are interested in learning more about our vision, exploring potential collaboration, or discussing investment opportunities, we invite you to connect with our team.

You can learn more about our company on our About Us page, meet the people building the project on the Meet the Team page, or reach out directly through our Contact Us page to start a conversation.

Disclaimer: The content published on this website is provided for informational purposes only and should not be interpreted as financial, investment, or regulatory advice.

Related Posts

Continue Reading

Fund Infrastructure & Tax

07: Tokenisation x HMRC

The FCA is progressing fund tokenisation and HMRC is refining DeFi tax approaches. Here is what both directions imply for onchain collateral and compliant markets.

Continue reading: 07: Tokenisation x HMRCSettlement Infrastructure

06: Atomic settlement in central bank money x RTGS synchronisation

The Bank is building RTGS synchronisation to enable atomic settlement in central bank money, including DSS digital securities transactions. Here is what is happening in 2026.

Continue reading: 06: Atomic settlement in central bank money x RTGS synchronisationMarket Structure

05: Tokenised gilts and DIGIT: the missing link in compliant RWA settlement

DIGIT is the UK's digital gilt pilot inside the Digital Securities Sandbox. Here is what is being tested: on-chain settlement, OTC functionality, interoperability and transparency.

Continue reading: 05: Tokenised gilts and DIGIT: the missing link in compliant RWA settlementNewsletter

Get New Research In Your Inbox

When we publish a new article, you will be the first to know.