Fund Infrastructure & Tax

07: Tokenisation x HMRC

The FCA is progressing fund tokenisation and HMRC is refining DeFi tax approaches. Here is what both directions imply for onchain collateral and compliant markets.

Newsletter

Get New Research In Your Inbox

When we publish a new article, you will be the first to know.

Tokenisation x HMRC

The financial industry is undergoing a profound transformation as technology, regulation, and investor expectations continue to evolve. At Liquida, we closely follow these developments while building solutions designed to address some of the most persistent inefficiencies in modern financial markets.

Our team is focused on understanding where the industry is heading and how emerging platforms, technologies, and investment models will shape the next decade of financial infrastructure. You can learn more about our mission and the team behind the project on our About Us page.

What the FCA is actually trying to enable

Most discussions around tokenisation tend to focus on technical infrastructure, particularly in relation to settlement and custody. However, for institutional adoption, the more binding constraints lie elsewhere. Two considerations consistently emerge as more decisive:

First, the availability of regulated wrappers, specifically, whether tokenised assets can be accommodated within established fund structures. Second, tax clarity, how these activities are characterised and treated from an economic and legal perspective. The Financial Conduct Authority’s work on fund tokenisation is focused on extending existing regulatory frameworks into digital environments, while HMRC’s evolving approach to DeFi taxation seeks to align treatment with the underlying economic substance of transactions.

Taken together, these developments begin to shift on-chain finance from something that is merely technically feasible to something that is operationally viable within institutional settings. Importantly, the FCA is not attempting to redesign the fund model. Its objective is to adapt existing structures, such as UCITS and authorised funds, so they can operate effectively within distributed or digitally native infrastructures.

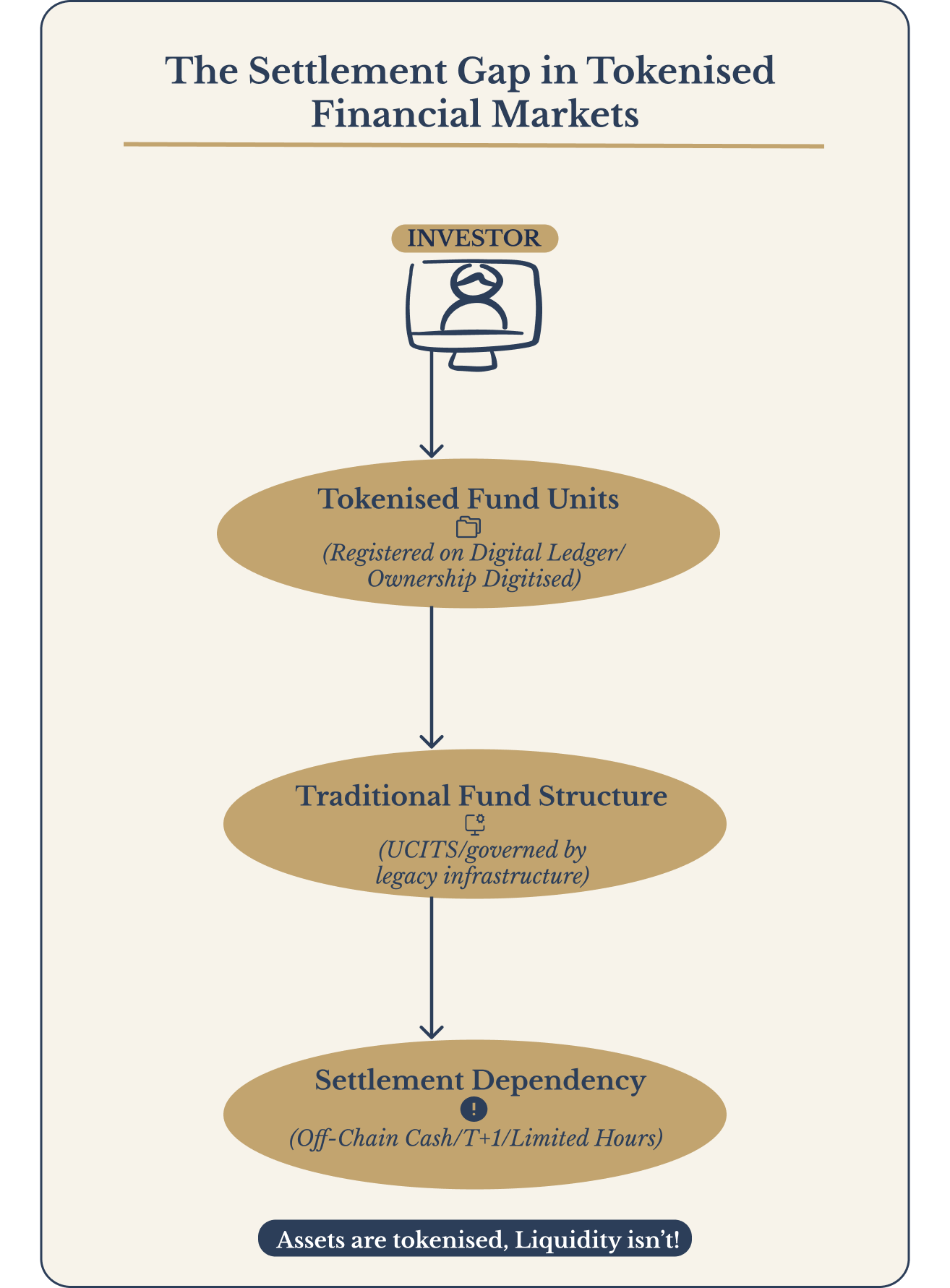

This includes a number of clearly stated goals: improving operational efficiency, enabling faster settlement, supporting new distribution models, and facilitating more programmable interactions between investors and fund structures. At the same time, the FCA explicitly recognises a set of practical constraints. These include dependencies on settlement mechanisms, the current absence of sufficiently robust on-chain cash instruments, and ongoing interoperability challenges between systems.

Across UK policy, a consistent theme is emerging: tokenised assets cannot operate in isolation. Their viability depends on the development of compatible forms of digital money and settlement infrastructure.

The FCA Fund Tokenisation Stack

What has actually been approved?

The FCA’s Blueprint model provides a useful reference point for how fund tokenisation is developing in practice. In January 2025, the FCA authorised a tokenised UK UCITS fund under this framework. This is a significant proof point: it demonstrates that tokenisation can be implemented within existing regulatory structures, without the need for an entirely new regime. However, the FCA is equally clear on the limitations of the current model.

More advanced implementations - particularly those that involve automated settlement, interoperability with digital asset markets, or programmable interactions - depend on the availability of on-chain cash instruments. In practice, this refers to mechanisms such as regulated stablecoins or tokenised deposits. This introduces a structural dependency within the emerging architecture. Tokenised funds, on their own, do not constitute a fully digital financial system, their functionality is constrained unless they can interact with a compatible form of digital money.

In simplified terms:

Tokenised funds

+

Digital money

=

Composable on-chain financial system

Without this second layer, tokenisation remains incomplete. Assets may be digitised at the registry or ownership level, but they cannot fully participate in atomic settlement or broader on-chain financial interactions.

Government-backed industry work: tokens as collateral

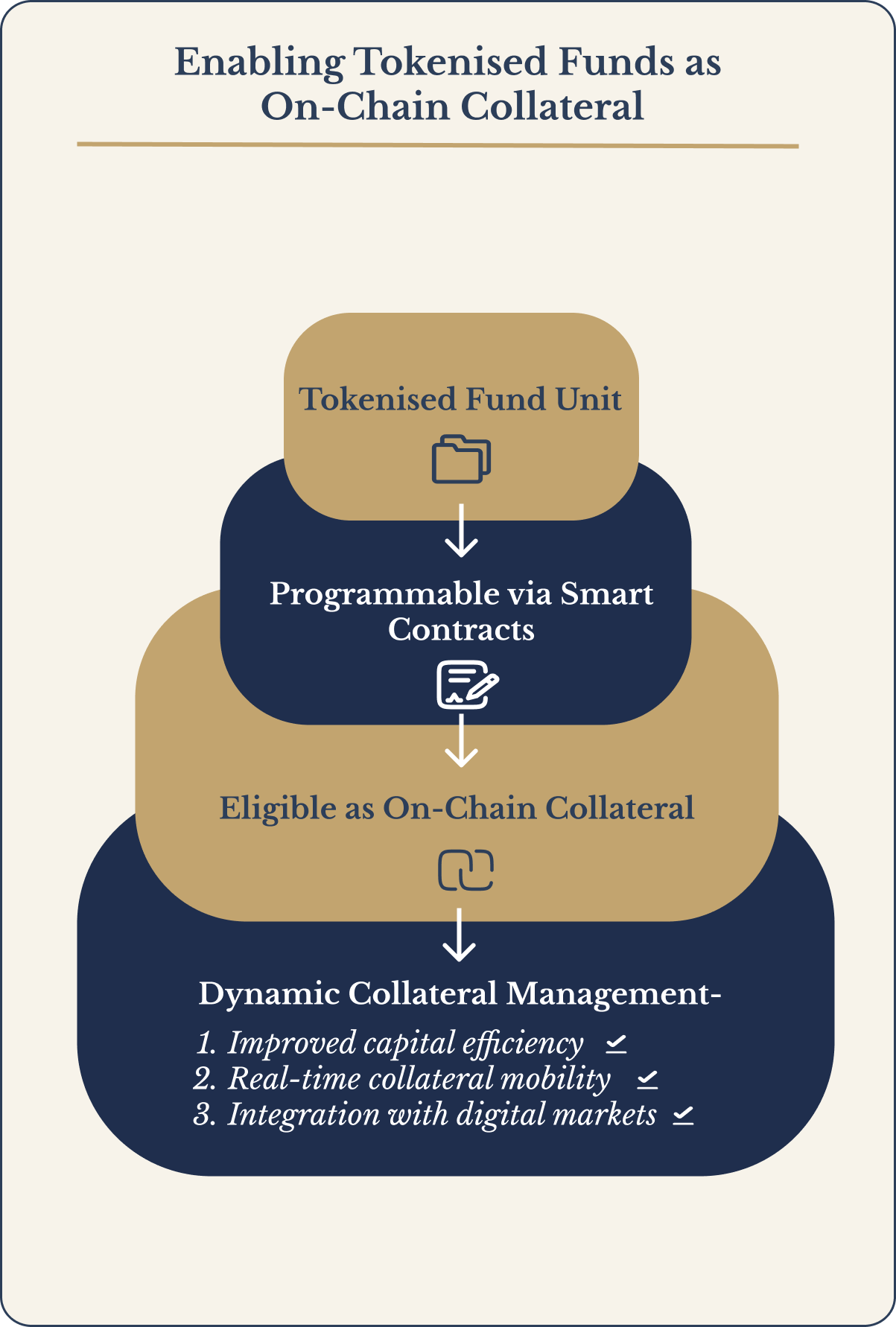

The UK’s Technology Working Group (TWG) has extended the discussion beyond tokenisation as a tool for operational efficiency. Its work increasingly points toward the emergence of new financial behaviours enabled by digital infrastructure. One of the most significant developments in this context is the use of tokenised fund units as collateral.

This marks a shift in how fund assets can be utilised within the financial system. Traditionally, fund units are held as relatively static instruments, with limited flexibility once allocated within a portfolio. Their role is primarily directional—providing exposure to underlying assets rather than serving as active components within broader liquidity or financing structures.

Tokenisation introduces a different paradigm. By representing fund units on programmable infrastructure, these assets can be integrated into collateral frameworks that support more dynamic financial activity. This includes the potential for real-time margining, automated collateral management, and more responsive liquidity provision.

In this sense, tokenised funds are not simply a more efficient wrapper for existing assets. They begin to function as programmable collateral, capable of interacting with other components of digital financial markets in ways that are not feasible within traditional systems.

Tokenised Funds as On-Chain Collateral

We believe that the next wave of financial innovation will come from companies that combine deep market understanding with scalable technology. Our team is actively working toward building a platform designed to unlock new opportunities within the financial ecosystem.

For those interested in the people and ideas behind this initiative, you can explore the background of our team on our Meet the Team page.

The tax layer: what HMRC is actually saying

This is often where otherwise well-designed tokenisation strategies encounter their most significant constraints. A common assumption among teams is that on-chain activity constitutes a fundamentally new category of financial interaction, and should therefore be treated as such from a tax perspective. HMRC’s current approach suggests the opposite.

Rather than focusing on the technical implementation, the emerging framework places emphasis on economic substance over form. In practical terms, this means that tax treatment is determined by what a transaction represents economically, rather than the mechanism through which it is executed.

This distinction has important implications. Activities such as lending, staking, or liquidity provision are unlikely to be treated as novel constructs simply because they occur on distributed infrastructure. Instead, they will be analysed through existing tax concepts, including distinctions between income and capital, and considerations of beneficial ownership versus custodial arrangements.

Alongside this, HMRC is exploring more specific frameworks to address edge cases. One example is the potential application of No Gain No Loss (NGNL) treatment for certain DeFi interactions, where assets are transferred or restructured without a clear realisation event in economic terms.

The significance of this should not be understated, without sufficient tax clarity, institutional participation remains constrained. Fund structures cannot allocate capital with confidence, and product design becomes inherently limited by uncertainty around treatment and reporting. In this sense, tax is not a secondary consideration. It is a foundational layer in determining whether on-chain financial models can operate at scale within regulated markets.

The Full Stack: Fund Tokenisation + Settlement + Tax

The real insight: the system is becoming legible

The UK is not simply enabling tokenisation as a technical capability, it is progressively shaping an environment in which on-chain financial activity can be understood, supervised, and integrated within existing institutional frameworks. In practical terms, this means making such activity regulatable, taxable, and auditable.

Institutional capital does not depend solely on technical feasibility; it depends on clarity - around legal treatment, risk, reporting, and enforceability. Without these foundations, on-chain finance remains experimental, confined to environments where uncertainty can be tolerated.

As these layers begin to solidify, the nature of the opportunity changes. What was previously a set of isolated technical experiments starts to resemble a coherent financial system, capable of supporting scale.

In this sense, the UK’s approach is less about accelerating innovation at all costs, and more about ensuring that when it does scale, it does so on terms that are compatible with the broader financial system.

FAQ

Can tokenised funds use stablecoins for settlement?

Potentially yes, but only if those stablecoins meet regulatory requirements.

The FCA has explicitly noted that on-chain cash instruments are required for more advanced models.

What is HMRC’s NGNL concept?

NGNL (No Gain No Loss) is being explored as a way to treat certain DeFi transactions:

- as neutral transfers

- rather than taxable disposals

This is still evolving but highly relevant for product design.

What should founders document for compliance?

At a minimum:

- economic intent of transactions

- ownership structures

- custody arrangements

- revenue generation mechanisms

Because tax treatment will follow economic substance, not code structure.

If you are interested in learning more about our vision, exploring potential collaboration, or discussing investment opportunities, we invite you to connect with our team.

You can learn more about our company on our About Us page, meet the people building the project on the Meet the Team page, or reach out directly through our Contact Us page to start a conversation.

Disclaimer: The content published on this website is provided for informational purposes only and should not be interpreted as financial, investment, or regulatory advice.

Related Posts

Continue Reading

Market Structure & Digital Money

08: The global banking pivot: why tokenised deposits and compliant stablecoins are the emerging mainstream

Major banks are testing stablecoins and tokenised deposits. Here is what that trend means for the UK regulatory direction, settlement infrastructure, and the future of onchain finance.

Continue reading: 08: The global banking pivot: why tokenised deposits and compliant stablecoins are the emerging mainstreamSettlement Infrastructure

06: Atomic settlement in central bank money x RTGS synchronisation

The Bank is building RTGS synchronisation to enable atomic settlement in central bank money, including DSS digital securities transactions. Here is what is happening in 2026.

Continue reading: 06: Atomic settlement in central bank money x RTGS synchronisationMarket Structure

05: Tokenised gilts and DIGIT: the missing link in compliant RWA settlement

DIGIT is the UK's digital gilt pilot inside the Digital Securities Sandbox. Here is what is being tested: on-chain settlement, OTC functionality, interoperability and transparency.

Continue reading: 05: Tokenised gilts and DIGIT: the missing link in compliant RWA settlementNewsletter

Get New Research In Your Inbox

When we publish a new article, you will be the first to know.