Market Structure

05: Tokenised gilts and DIGIT: the missing link in compliant RWA settlement

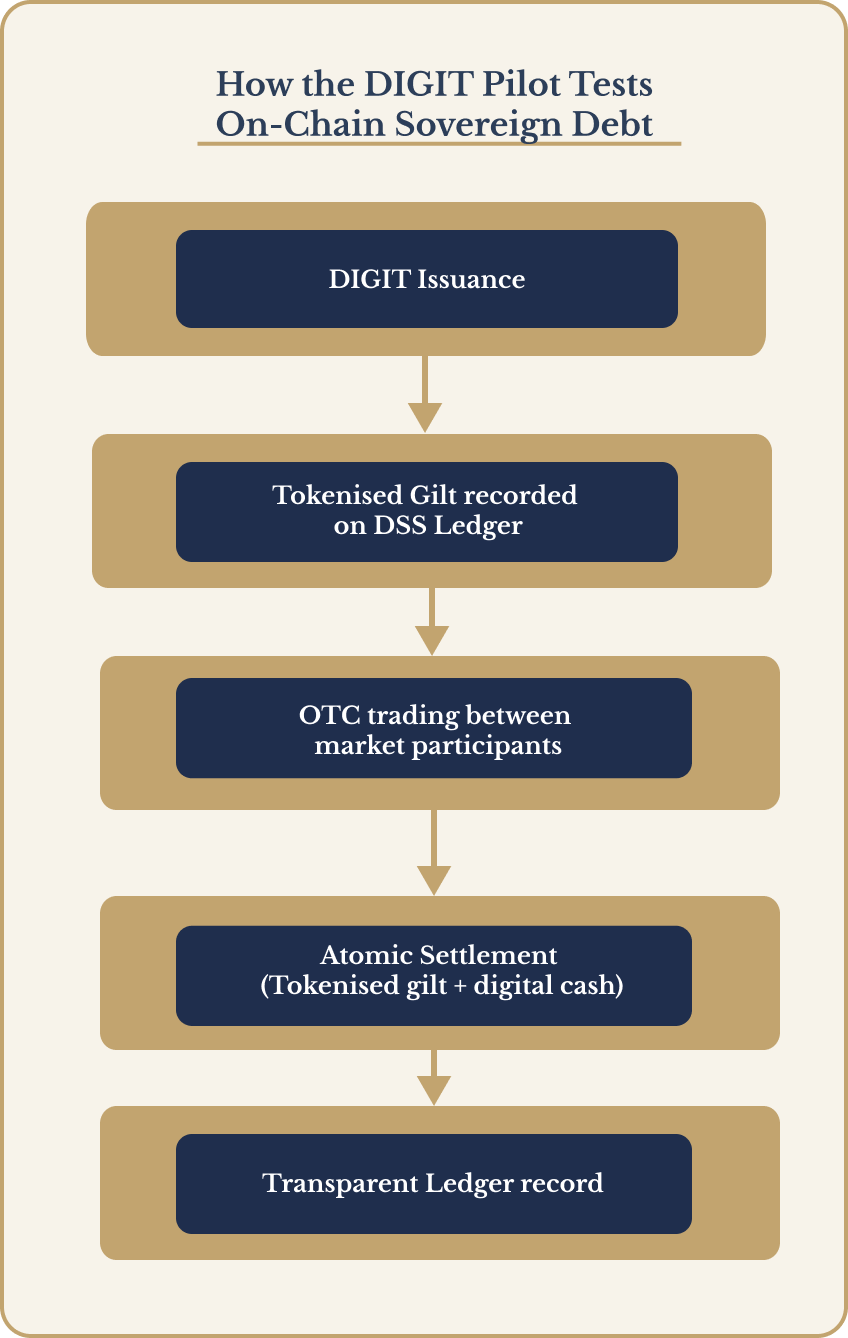

DIGIT is the UK's digital gilt pilot inside the Digital Securities Sandbox. Here is what is being tested: on-chain settlement, OTC functionality, interoperability and transparency.

Newsletter

Get New Research In Your Inbox

When we publish a new article, you will be the first to know.

Tokenised gilts and DIGIT: the missing link in compliant RWA settlement

The financial industry is undergoing a profound transformation as technology, regulation, and investor expectations continue to evolve. At Liquida, we closely follow these developments while building solutions designed to address some of the most persistent inefficiencies in modern financial markets.

Our team is focused on understanding where the industry is heading and how emerging platforms, technologies, and investment models will shape the next decade of financial infrastructure. You can learn more about our mission and the team behind the project on our About Us page.

What the DIGIT is

The UK government is preparing to issue a digitally native government bond as part of the Digital Securities Sandbox (DSS). The instrument is known as DIGIT (the Digital Gilt Instrument), it is not a tokenised version of an existing government bond.

DIGIT will be:

- digitally native

- short-dated

- issued within the Digital Securities Sandbox

- separate from the UK’s conventional gilt issuance programme

The goal is to test whether distributed ledger technology can support sovereign debt issuance and settlement inside regulated market infrastructure. The DIGIT is a policy experiment, and could potentially be a permanent product to sell sovereign debt, as the infrastructure tested through the pilot could shape how sovereign debt markets evolve in the future.

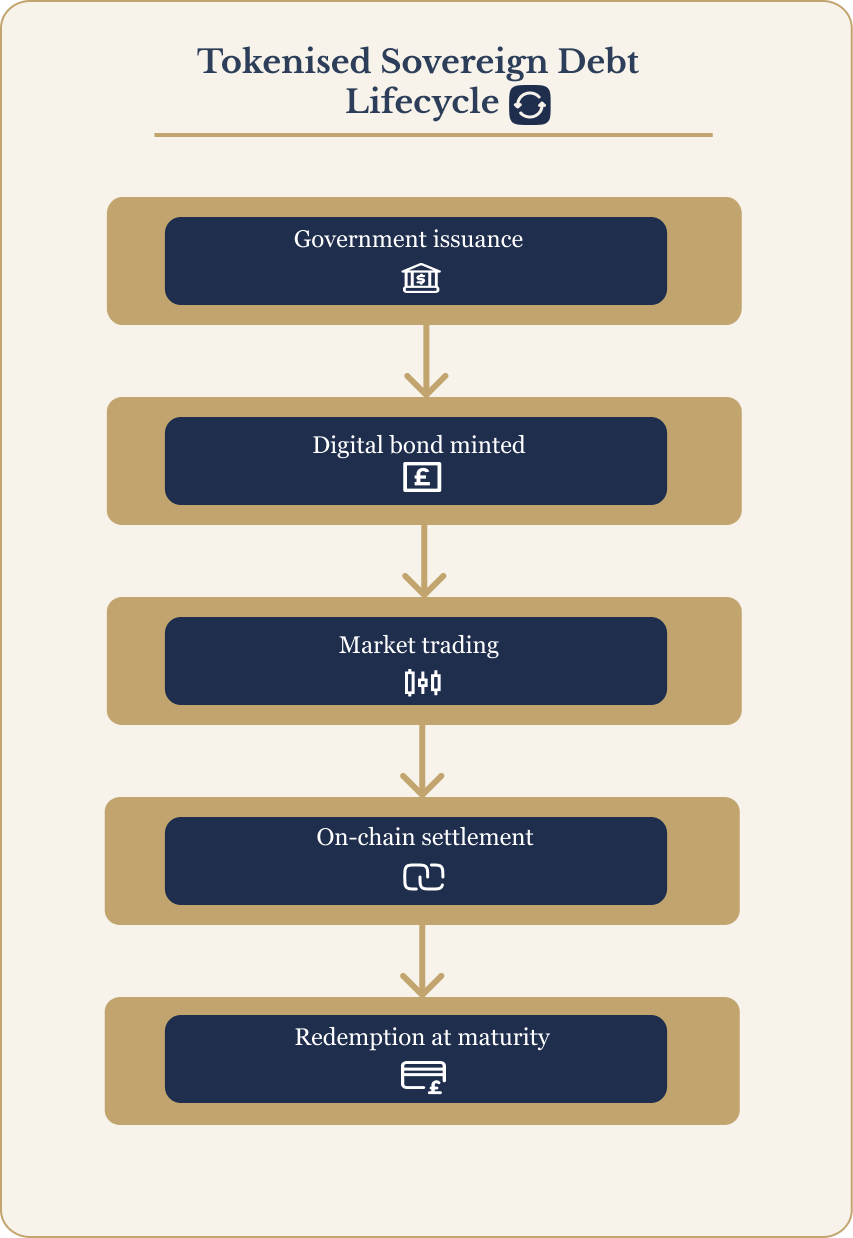

Sovereign Debt Lifecycle

What the pilot will actually test

The DIGIT pilot focuses on several practical market functions; these experiments are designed to evaluate whether tokenised sovereign debt can operate safely inside existing financial markets. The areas being tested include:

On-chain settlement

One of the most significant tests is whether a government bond can settle directly on distributed ledger infrastructure.

This includes settlement of both:

- the security leg (ownership of the gilt)

- the cash leg (payment)

Reducing settlement complexity is a major motivation and traditional bond settlement typically relies on multiple intermediaries and delayed clearing processes. Tokenised settlement could enable near-instant settlement with atomic execution.

OTC trading and settlement

Another area of testing involves over-the-counter (OTC) trading workflows. Many government bond transactions occur outside central exchanges through dealer networks.

The pilot will examine whether:

- tokenised bonds can support OTC trading structures

- settlement can be automated through smart contracts

- ownership transfers can be recorded transparently on ledger infrastructure

Interoperability

Interoperability will determine whether tokenised markets remain niche experiments or become integrated into global financial infrastructure. A key regulatory objective is ensuring that tokenised assets can interact with existing financial market infrastructure. This includes compatibility with:

- traditional settlement systems

- regulated trading venues

- other distributed ledger platforms

Transparency

Distributed ledger systems can provide shared transaction records across market participants. For sovereign debt markets, where transparency and trust are essential, this could be particularly valuable. The pilot will explore whether this transparency can improve:

- settlement confidence

- market monitoring

- regulatory oversight

The DIGIT settlement experiment

We believe that the next wave of financial innovation will come from companies that combine deep market understanding with scalable technology. Our team is actively working toward building a platform designed to unlock new opportunities within the financial ecosystem.

For those interested in the people and ideas behind this initiative, you can explore the background of our team on our Meet the Team page.

Why tokenised sovereign debt could become a foundational RWA primitive

Government bonds sit at the centre of modern financial markets, they are widely used as:

- collateral in repo markets

- liquidity management instruments

- reference assets for pricing financial products

Tokenising sovereign debt could unlock several structural improvements;

Faster settlement: Settlement times could move from days to minutes, reducing counterparty risk.

Collateral mobility: Tokenised bonds could move more easily between platforms, improving collateral efficiency across markets.

Transparency: Shared ledgers could provide regulators and institutions with clearer transaction records.

Reduced market fragmentation: If tokenised bonds can interoperate across infrastructures, it may reduce fragmentation between trading venues and settlement systems.

Importantly, these benefits do not require replacing existing markets, only upgrading settlement infrastructure.

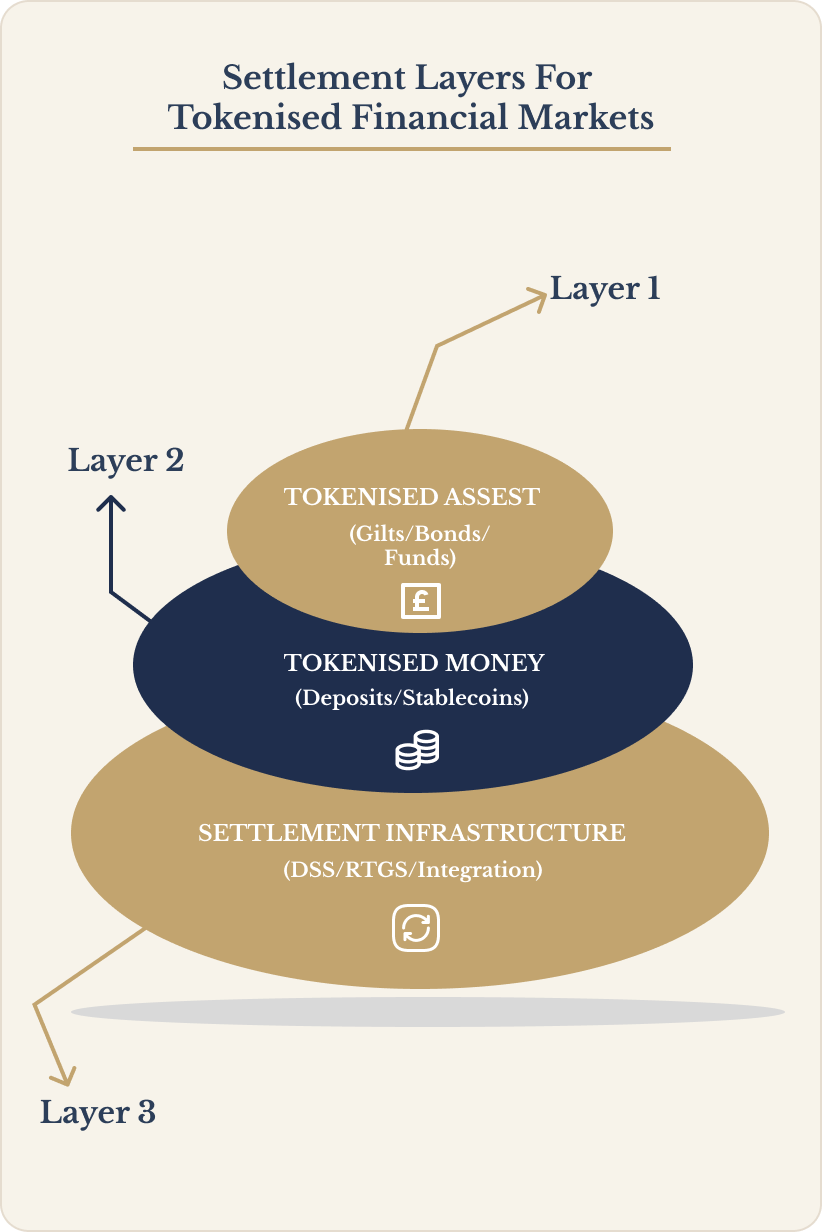

The settlement-money question

A key question in all tokenised asset experiments is, what form of money will be used to settle transactions? Regulators frequently reference two potential options for wholesale markets:

Tokenised deposits: Commercial banks may issue tokenised representations of bank deposits that can settle transactions on distributed ledgers.

Regulated stablecoins: Systemic stablecoins could potentially act as settlement assets within regulated tokenised financial markets.

This is one reason the Bank of England frequently discusses stablecoins, tokenised deposits, and the Digital Securities Sandbox together. Tokenised assets require compatible digital money in order to settle efficiently.

Tokenised Asset Settlement Stack

Why regulators are starting with sovereign debt

Sovereign bonds are a logical starting point for tokenisation experiments, they combine several important characteristics:

- deep liquidity

- strong legal frameworks

- global investor demand

Testing tokenisation with sovereign debt allows regulators to evaluate distributed ledger infrastructure without introducing unnecessary credit risk. In this sense, DIGIT may represent the first step toward broader real-world asset tokenisation in regulated markets.

FAQ

When will DIGIT be issued?

The UK government has indicated that DIGIT issuance is expected during the Digital Securities Sandbox testing window, although precise timelines depend on regulatory and infrastructure readiness.

Will DIGIT settle against tokenised money?

One of the objectives of the pilot is to explore how tokenised securities interact with digital settlement assets, which could include tokenised deposits or regulated stablecoins.

Could DIGIT affect UK capital markets infrastructure?

Potentially. If tokenised sovereign debt proves operationally viable, it could influence how:

- securities settlement systems operate

- collateral moves between financial institutions

- digital asset markets integrate with traditional finance

However, the current pilot remains a controlled regulatory experiment.

Why this matters for the future of financial infrastructure

Tokenisation discussions often focus on private assets or speculative crypto markets, the DIGIT reflects a different direction, It shows regulators testing whether core financial market infrastructure can evolve using distributed ledger technology. If successful, tokenised sovereign debt could become one of the most important building blocks for regulated real-world asset markets. And that may ultimately prove more transformative than any individual digital asset.

If you are interested in learning more about our vision, exploring potential collaboration, or discussing investment opportunities, we invite you to connect with our team.

You can learn more about our company on our About Us page, meet the people building the project on the Meet the Team page, or reach out directly through our Contact Us page to start a conversation.

Disclaimer: The content published on this website is provided for informational purposes only and should not be interpreted as financial, investment, or regulatory advice.

Related Posts

Continue Reading

Market Structure & Digital Money

08: The global banking pivot: why tokenised deposits and compliant stablecoins are the emerging mainstream

Major banks are testing stablecoins and tokenised deposits. Here is what that trend means for the UK regulatory direction, settlement infrastructure, and the future of onchain finance.

Continue reading: 08: The global banking pivot: why tokenised deposits and compliant stablecoins are the emerging mainstreamFund Infrastructure & Tax

07: Tokenisation x HMRC

The FCA is progressing fund tokenisation and HMRC is refining DeFi tax approaches. Here is what both directions imply for onchain collateral and compliant markets.

Continue reading: 07: Tokenisation x HMRCSettlement Infrastructure

06: Atomic settlement in central bank money x RTGS synchronisation

The Bank is building RTGS synchronisation to enable atomic settlement in central bank money, including DSS digital securities transactions. Here is what is happening in 2026.

Continue reading: 06: Atomic settlement in central bank money x RTGS synchronisationNewsletter

Get New Research In Your Inbox

When we publish a new article, you will be the first to know.