Market Structure

04: Tokenised deposits vs stablecoins vs a digital pound: the UK multi-money future

A clear map of UK digital money: tokenised deposits, regulated stablecoins and the digital pound debate—where each fits in payments and settlement.

Newsletter

Get New Research In Your Inbox

When we publish a new article, you will be the first to know.

Tokenised deposits vs stablecoins vs a digital pound: the UK multi-money future

The financial industry is undergoing a profound transformation as technology, regulation, and investor expectations continue to evolve. At Liquida, we closely follow these developments while building solutions designed to address some of the most persistent inefficiencies in modern financial markets.

Our team is focused on understanding where the industry is heading and how emerging platforms, technologies, and investment models will shape the next decade of financial infrastructure. You can learn more about our mission and the team behind the project on our About Us page.

The UK’s multi-money system and why regulators keep using this phrase

If you read the Bank of England’s recent consultations on digital money, one phrase appears repeatedly: The UK is moving toward a multi-money system. This framing is important as it signals that the policymakers are not trying to replace existing forms of money with a single digital solution. Instead, the BoE expects several types of digital money to coexist, each with different roles in the financial system.

In practice, three forms of digital sterling are emerging:

- Tokenised bank deposits

- Regulated stablecoins

- A potential digital pound (central bank digital currency)

Each form of money carries different legal protections, settlement properties, and governance models. Understanding the differences is essential for anyone building payment infrastructure, digital asset platforms, or tokenised financial markets in the UK.

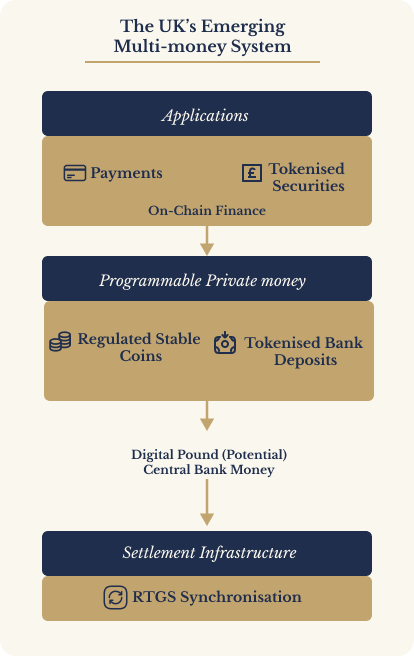

The UK Multi-Money Stack

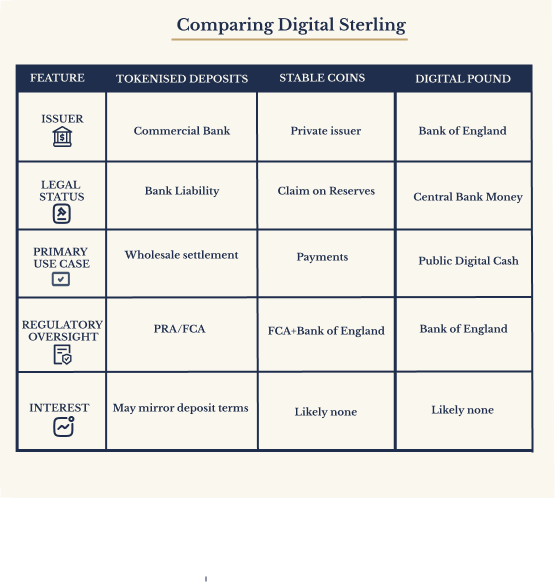

Tokenised sterling deposits (GBTD): what banks are piloting

Tokenised deposits are essentially traditional bank deposits represented in digital form on distributed ledgers. They remain liabilities of commercial banks, meaning they carry the same fundamental legal status as deposits in a bank account. One of the most visible initiatives in this space is the GBTD (Global Bank Tokenised Deposit) project coordinated by UK Finance. The initiative brings together major financial institutions to explore how tokenised deposits could support:

- programmable payments

- tokenised securities settlement

- cross-institution settlement networks

The project also connects to broader experiments such as the Regulated Liability Network (RLN), which explores how tokenised central bank money and tokenised deposits might interoperate. The goal is not to create new money, It is to make existing bank money programmable and interoperable with digital asset infrastructure. Potential use cases include:

- wholesale financial market settlement

- tokenised securities trading

- automated payment flows between financial institutions

For banks, tokenised deposits represent a way to modernise existing payment rails without fundamentally changing the monetary system.

Regulated stablecoins: private digital money for payments

Stablecoins differ from tokenised deposits, they are not bank liabilities, they are issued by private entities and backed by reserve assets held in custody. The UK regulatory approach is evolving toward a regime where regulated stablecoins are designed primarily for payments. The Bank of England and the FCA are attempting to ensure several key safeguards, The points below allows for innovation in payments without undermining the trust in the broader monetary system.

Par redemption: Users must be able to redeem stablecoins at par value. This ensures the token functions as a reliable payment instrument rather than a speculative asset.

Backing asset safeguards: Reserve assets must be held in safe, liquid sterling instruments such as bank deposits or UK government securities.

Transition holding limits: Early proposals include holding limits for individuals as a transitional measure, helping prevent sudden migration of bank deposits into stablecoins.

Regulatory supervision: Systemic stablecoins would be supervised jointly by the Bank of England and the FCA, this ensures both financial stability and consumer protection concerns are addressed.

Digital pound: public digital money

The third pillar of the UK’s digital money landscape is the potential digital pound. Unlike stablecoins or tokenised deposits, a digital pound would be central bank money issued directly by the Bank of England. This would make it comparable to physical cash, but in digital form. However, policymakers have been cautious, the current discussions are that a digital pound would likely include holding limits, ensuring it complements rather than replaces commercial bank deposits.

The digital pound debate focuses on questions such as:

- financial inclusion

- resilience of the payments system

- public access to central bank money in a digital economy

It is not trying to replace private payment innovation, it would likely coexist with both stablecoins and tokenised deposits within the multi-money ecosystem.

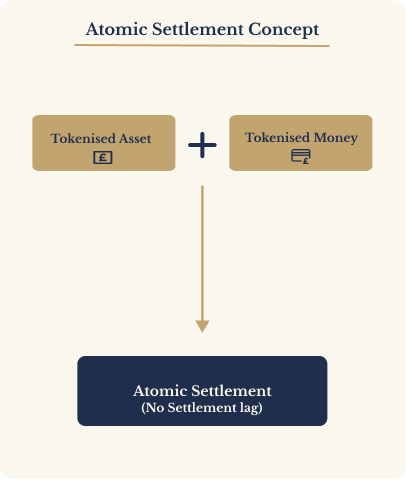

Why interoperability and atomic settlement keep appearing in policy discussions

Across multiple consultations and industry initiatives, regulators are repeatedly highlighting two ideas, interoperability and atomic settlement. Interoperability refers to the ability of different forms of digital money to operate seamlessly across platforms and networks. Atomic settlement refers to a transaction structure where two assets exchange simultaneously, eliminating settlement risk.

Atomic Settlement

This becomes important in tokenised financial markets, as securities are issued and traded on distributed ledgers, settlement assets must be able to operate within the same environment. That is why initiatives such as RTGS synchronisation are being explored. The Bank of England is studying how the existing Real-Time Gross Settlement system (RTGS) could interact with distributed ledger infrastructure. The long-term goal is to enable digital assets, tokenised money and traditional financial infrastructure to interoperate safely.

We believe that the next wave of financial innovation will come from companies that combine deep market understanding with scalable technology. Our team is actively working toward building a platform designed to unlock new opportunities within the financial ecosystem.

For those interested in the people and ideas behind this initiative, you can explore the background of our team on our Meet the Team page.

Three Forms of Digital Sterling

FAQ

Are tokenised deposits on-chain money?

They can be, tokenised deposits represent bank liabilities that are recorded and transferred using distributed ledger infrastructure. However, they remain fundamentally the same as traditional bank deposits from a legal perspective.

Do stablecoins receive deposit protection?

No. Stablecoins are not bank deposits and typically do not benefit from deposit protection schemes. Instead, their safety relies on reserve asset structures and regulatory safeguards.

What role does RTGS play in digital money?

RTGS remains the core settlement infrastructure for central bank money in the UK. Future initiatives aim to allow RTGS to synchronise with distributed ledger networks, enabling safe settlement between traditional and tokenised financial systems.

Why the multi-money model matters

The UK is not trying to pick a single winner in the digital money debate. Instead, policymakers are designing a system where multiple forms of digital sterling coexist, each serving different functions in the economy. This approach reflects a broader principle of financial systems evolving through layered innovation, not wholesale replacement. Tokenised deposits modernise bank money, stablecoins enable new payment networks, and a digital pound could provide public digital cash. Together, they form the foundations of the next generation of financial infrastructure.

If you are interested in learning more about our vision, exploring potential collaboration, or discussing investment opportunities, we invite you to connect with our team.

You can learn more about our company on our About Us page, meet the people building the project on the Meet the Team page, or reach out directly through our Contact Us page to start a conversation.

Disclaimer: The content published on this website is provided for informational purposes only and should not be interpreted as financial, investment, or regulatory advice.

Related Posts

Continue Reading

Market Structure & Digital Money

08: The global banking pivot: why tokenised deposits and compliant stablecoins are the emerging mainstream

Major banks are testing stablecoins and tokenised deposits. Here is what that trend means for the UK regulatory direction, settlement infrastructure, and the future of onchain finance.

Continue reading: 08: The global banking pivot: why tokenised deposits and compliant stablecoins are the emerging mainstreamFund Infrastructure & Tax

07: Tokenisation x HMRC

The FCA is progressing fund tokenisation and HMRC is refining DeFi tax approaches. Here is what both directions imply for onchain collateral and compliant markets.

Continue reading: 07: Tokenisation x HMRCSettlement Infrastructure

06: Atomic settlement in central bank money x RTGS synchronisation

The Bank is building RTGS synchronisation to enable atomic settlement in central bank money, including DSS digital securities transactions. Here is what is happening in 2026.

Continue reading: 06: Atomic settlement in central bank money x RTGS synchronisationNewsletter

Get New Research In Your Inbox

When we publish a new article, you will be the first to know.