Regulatory Insights

03: Sterling systemic stablecoins and what the Bank is actually proposing

Backing assets, redemption, holding limits and liquidity backstops—what the Bank of England is proposing for sterling-denominated systemic stablecoins.

Newsletter

Get New Research In Your Inbox

When we publish a new article, you will be the first to know.

Sterling systemic stablecoins: what the Bank of England is actually proposing

The financial industry is undergoing a profound transformation as technology, regulation, and investor expectations continue to evolve. At Liquida, we closely follow these developments while building solutions designed to address some of the most persistent inefficiencies in modern financial markets.

Our team is focused on understanding where the industry is heading and how emerging platforms, technologies, and investment models will shape the next decade of financial infrastructure. You can learn more about our mission and the team behind the project on our About Us page.

The point of this regime: make stablecoins payments-native, not deposit-like

The Bank of England’s view on sterling-denominated stablecoins is easy to misread if you come at it like a crypto product spec, they already know how to launch a coin. It’s closer to a set of financial stability design constraints for a new form of money that, if it becomes widely used, could affect credit conditions, payment resilience, and confidence in the UK monetary system. (Bank of England)

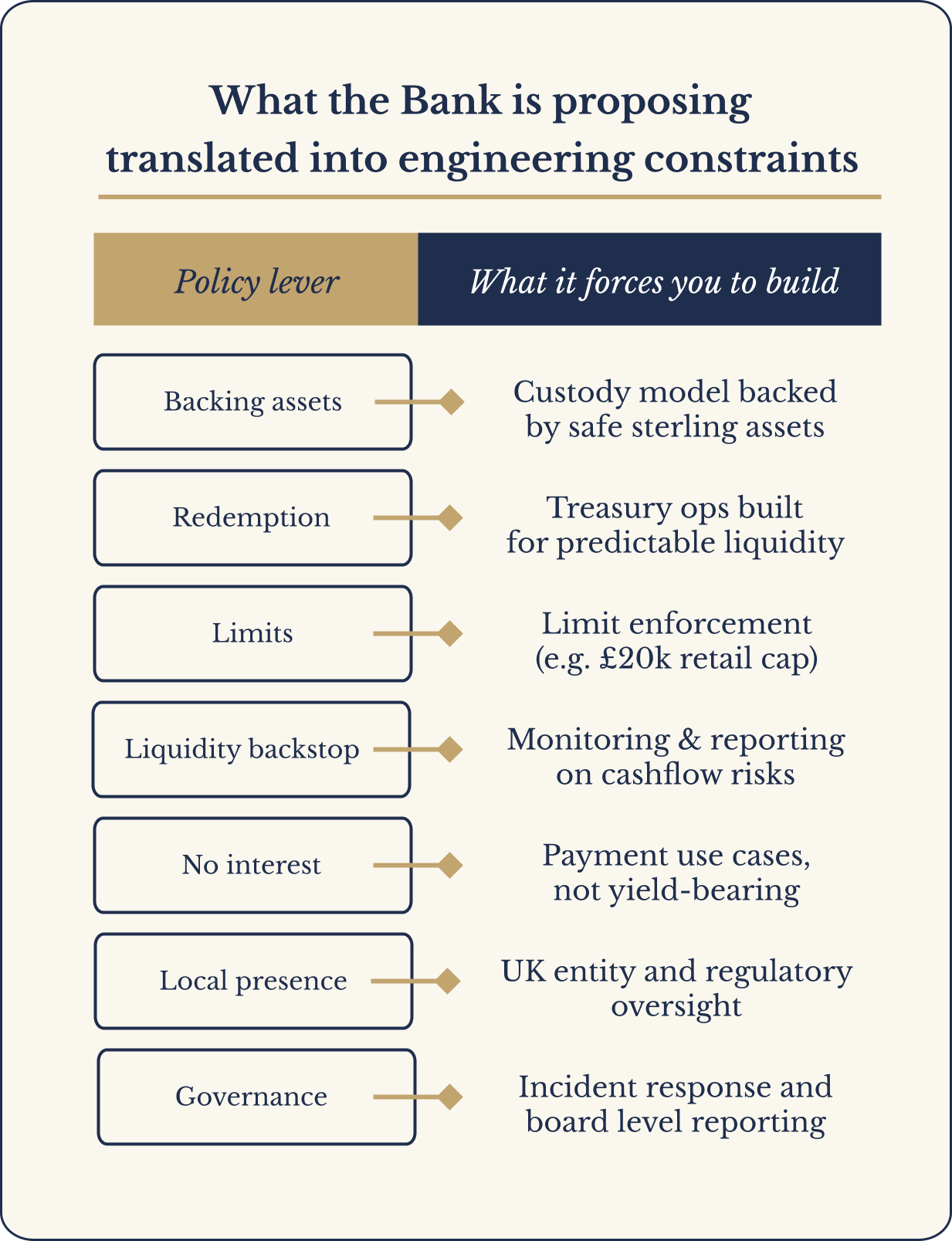

If you’re building (or investing in) a GBP stablecoin issuer, the practical question becomes, what does the Bank’s proposed regime force you to design for, operationally?

BoE’s Proposal

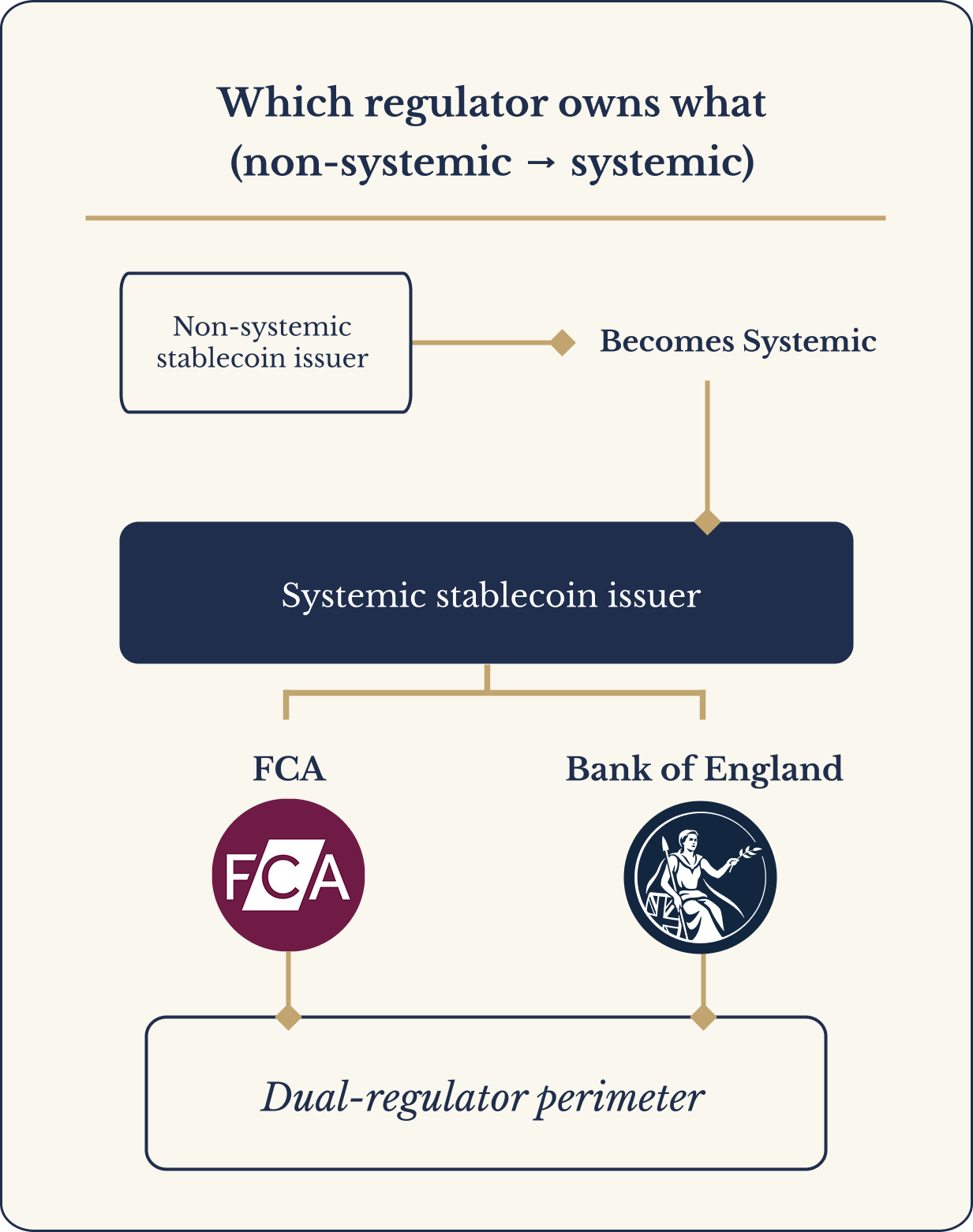

Systemic vs non-systemic: which stablecoins fall under the Bank vs the FCA

The proposed UK approach is a two-regulator model:

- FCA regulates stablecoin issuance and related activities for non-systemic use cases (and continues to supervise conduct and consumer protection even where a stablecoin becomes systemic). (FCA)

- Bank of England regulates stablecoins that HM Treasury recognises as systemic payment systems (or systemic service providers) focused on prudential, resilience, and financial stability outcomes. (Bank of England)

So systemic here is a recognition decision about whether disruption or deficiencies could threaten stability or confidence in the UK financial system. The design implication is you don’t choose BoE’s regulation, you scale into it, or you launch an already systemic and face a step-up approach from day one (Bank of England).

BoE’s Proposal

Backing assets: why the Bank moved from 100% deposits to a mixed model

The BoE’s earlier framing leaned towards extremely conservative backing approaches. In the newer consultation, the BoE proposes a more flexible, viability-aware approach while still treating backing assets as the core safety mechanism (Bank of England).

Two specific design constraints matter most:

1) The backing portfolio must be payments-safe

In plain terms: backing assets must be high-quality, liquid, sterling-denominated, and operationally set up so the issuer can meet redemptions under stress (not just in normal times). (Bank of England)

2) There’s an explicit step-up regime if you’re systemic at launch

The BoE proposes allowing an issuer recognised as systemic at launch to temporarily hold up to 95% of backing assets in sterling-denominated UK government securities, then reduce to 60% as the coin scales case by case (Bank of England). The design implication is the treasury function is not a side quest. Under this regime, backing assets and liquidity management are the product.

We believe that the next wave of financial innovation will come from companies that combine deep market understanding with scalable technology. Our team is actively working toward building a platform designed to unlock new opportunities within the financial ecosystem.

For those interested in the people and ideas behind this initiative, you can explore the background of our team on our Meet the Team page.

Redemption and legal claim: what redeem at par means operationally

Redeem at par sounds simple, but operationally, it’s the hardest part. The BoE’s regime is built around the idea that:

- A coin used for everyday payments must remain reliable money-like infrastructure.

- Redemptions must work smoothly under stress conditions, not only when markets are calm. (Bank of England)

A practical translation is you must engineer redemption as a system, not a feature:

- Clear legal claim structure for holders

- Reliable redemption processes and cutoffs

- Intraday liquidity planning (because payment flows don’t respect treasury hours)

- Contingency planning for runs and rapid outflows

The FCA’s parallel work on stablecoin issuance also emphasises robust redemption arrangements (consumer clarity, backing asset management and redemption policy), which becomes even more critical once systemic (FCA).

Holding limits as a transition tool, plus the DSS wholesale settlement carve-out

The BoE is explicitly managing the risk of rapid deposit outflows from banks into stablecoins disrupting the supply of credit to the real economy (Bank of England). One of the headline UK differences is holding limits, the BoE proposes temporary limits of:

- £20,000 per coin for individuals

- £10 million per coin for businesses, with exemptions for large businesses where needed (Bank of England)

The DSS carve-out

The BoE notes that stablecoins used as a settlement asset in high-value wholesale markets require different treatment, and it intends to explore this via the Digital Securities Sandbox (DSS) where holding limits do not apply (Bank of England). Retail payments and wholesale settlement are being treated as distinct regulatory products, even if the token is technically similar.

Payments, not an investment product: no interest to coinholders

The direction of travel is clear, a systemic retail stablecoin is being regulated as part of the payments ecosystem, not as a yield product. A core principle is that stablecoins used for payments should not be structured to behave like deposit substitutes that compete on yield. That is part of why:

- holding limits exist (initially)

- backing asset rules are strict

- the regime stresses operational resilience and payment reliability (Bank of England)

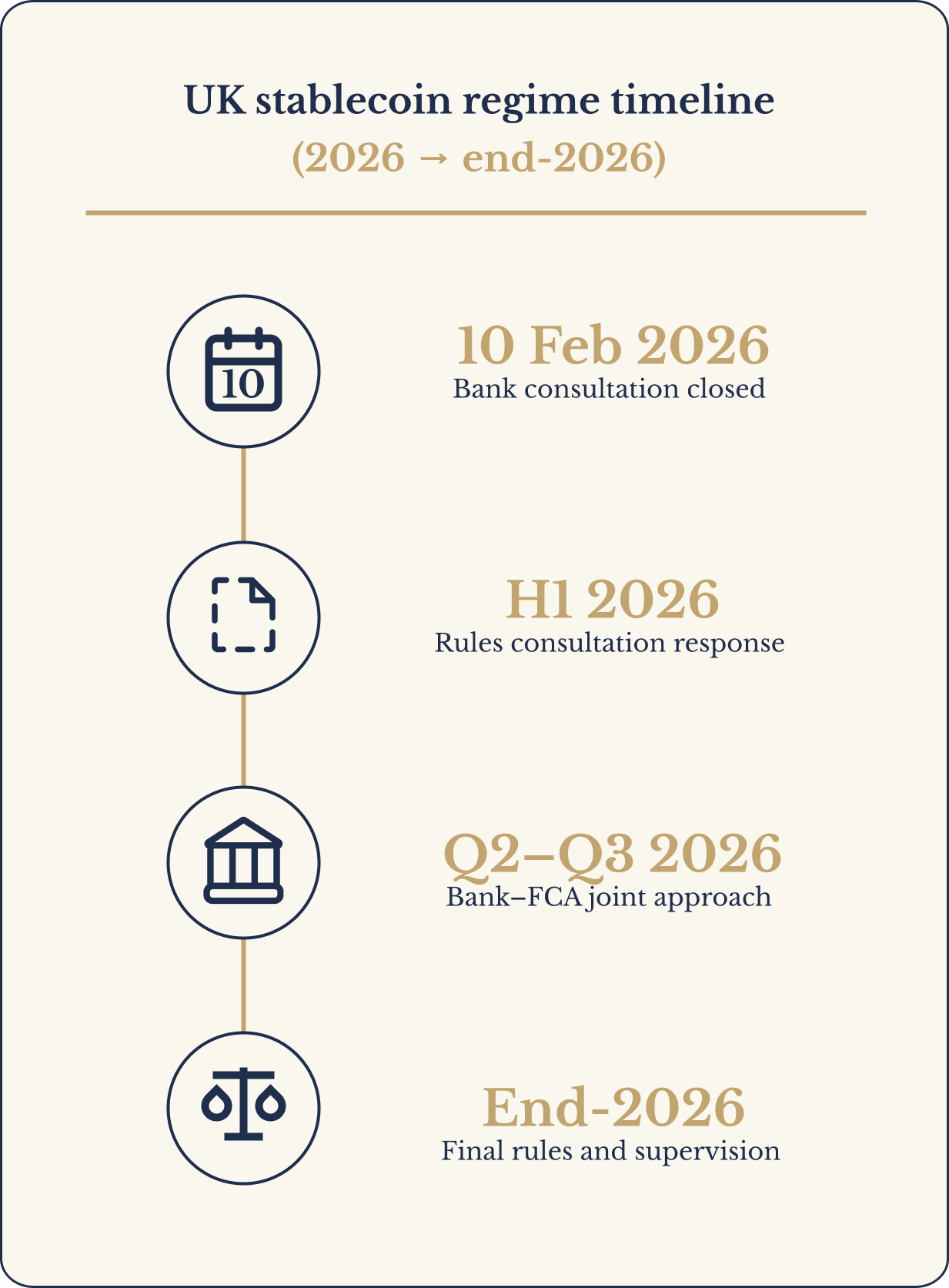

There’s also a separate, very practical industry point; payments stability often requires access to strong settlement rails and robust liquidity arrangements. The UK’s payments roadmap explicitly sequences stablecoin milestones across 2026 (BoE consultation closes, BoE rules consultation in H1 2026, final BoE rules end-2026, joint BoE-FCA approach in Q2–Q3 2026).

BoE’s Proposal

The issuer checklist: the BoE’s design constraints in one view

Here’s the simplest way to operationalise the consultation:

- Backed by safe sterling assets (not venture treasury vibes)

- Redeemable at par with real operational readiness

- Liquidity stress planning (including rapid outflow scenarios)

- Holding limits enforced (at least during transition)

- No yield coin positioning for payments use cases

- DSS-aware pathway for wholesale settlement use cases

- Dual-regulator readiness (BoE + FCA) for systemic operations (Bank of England)

FAQ

When does the BoE finalise the rules?

The BoE’s consultation closes 10 February 2026, with further rules consultation and response in H1 2026, and final rules / supervisory approach targeted for end-2026.

Can backing assets earn yield?

Yes backing assets like UK government securities yield. The key constraint is that the stablecoin is being treated as payments infrastructure, not an investment wrapper for coinholders, and the backing portfolio must be structured for redemption and resilience (Bank of England).

Do holding limits apply in wholesale markets?

The BoE explicitly signals that wholesale settlement stablecoin use cases will be explored via the DSS and that holding limits do not apply there (Bank of England).

If you are interested in learning more about our vision, exploring potential collaboration, or discussing investment opportunities, we invite you to connect with our team.

You can learn more about our company on our About Us page, meet the people building the project on the Meet the Team page, or reach out directly through our Contact Us page to start a conversation.

Disclaimer: The content published on this website is provided for informational purposes only and should not be interpreted as financial, investment, or regulatory advice.

Related Posts

Continue Reading

Market Structure & Digital Money

08: The global banking pivot: why tokenised deposits and compliant stablecoins are the emerging mainstream

Major banks are testing stablecoins and tokenised deposits. Here is what that trend means for the UK regulatory direction, settlement infrastructure, and the future of onchain finance.

Continue reading: 08: The global banking pivot: why tokenised deposits and compliant stablecoins are the emerging mainstreamFund Infrastructure & Tax

07: Tokenisation x HMRC

The FCA is progressing fund tokenisation and HMRC is refining DeFi tax approaches. Here is what both directions imply for onchain collateral and compliant markets.

Continue reading: 07: Tokenisation x HMRCSettlement Infrastructure

06: Atomic settlement in central bank money x RTGS synchronisation

The Bank is building RTGS synchronisation to enable atomic settlement in central bank money, including DSS digital securities transactions. Here is what is happening in 2026.

Continue reading: 06: Atomic settlement in central bank money x RTGS synchronisationNewsletter

Get New Research In Your Inbox

When we publish a new article, you will be the first to know.