Market Structure

09: How Do Repo Markets Work in the UK?

A research-driven guide to how the UK repo market works, including gilt collateral, settlement mechanics, market participants, and the Bank of England’s evolving resilience agenda.

Newsletter

Get New Research In Your Inbox

When we publish a new article, you will be the first to know.

UK Gilt Repo Market: Structure, Resilience Reforms, and What’s Changing

The financial industry is undergoing a profound transformation as technology, regulation, and investor expectations continue to evolve. At Liquida, we closely follow these developments while building solutions designed to address some of the most persistent inefficiencies in modern financial markets.

Our team is focused on understanding where the industry is heading and how emerging platforms, technologies, and investment models will shape the next decade of financial infrastructure. You can learn more about our mission and the team behind the project on our About Us page.

The gilt repo market is one of the core mechanisms through which liquidity moves across the UK financial system. It sits beneath government bond market functioning, dealer balance sheet management, collateral mobility, and short-term funding. It also sits close to the heart of financial stability. When UK authorities discuss market resilience in gilts, It is increasingly treated as part of the system’s core plumbing.

This is most visible in the Bank of England’s recent work, in September 2025, the Bank published a discussion paper on enhancing the resilience of the gilt repo market. In April 2026, it followed with a feedback statement summarising industry responses and signalling further work through 2026, with potential policy proposals expected in early 2027. That agenda makes the UK gilt repo market an active policy issue.

This article explains what a gilt repo is, how the market works, why resilience has become a priority, and what reforms are now under discussion.

Gilt Backed Borrowing

What “gilt repo” is and why it matters for UK market functioning

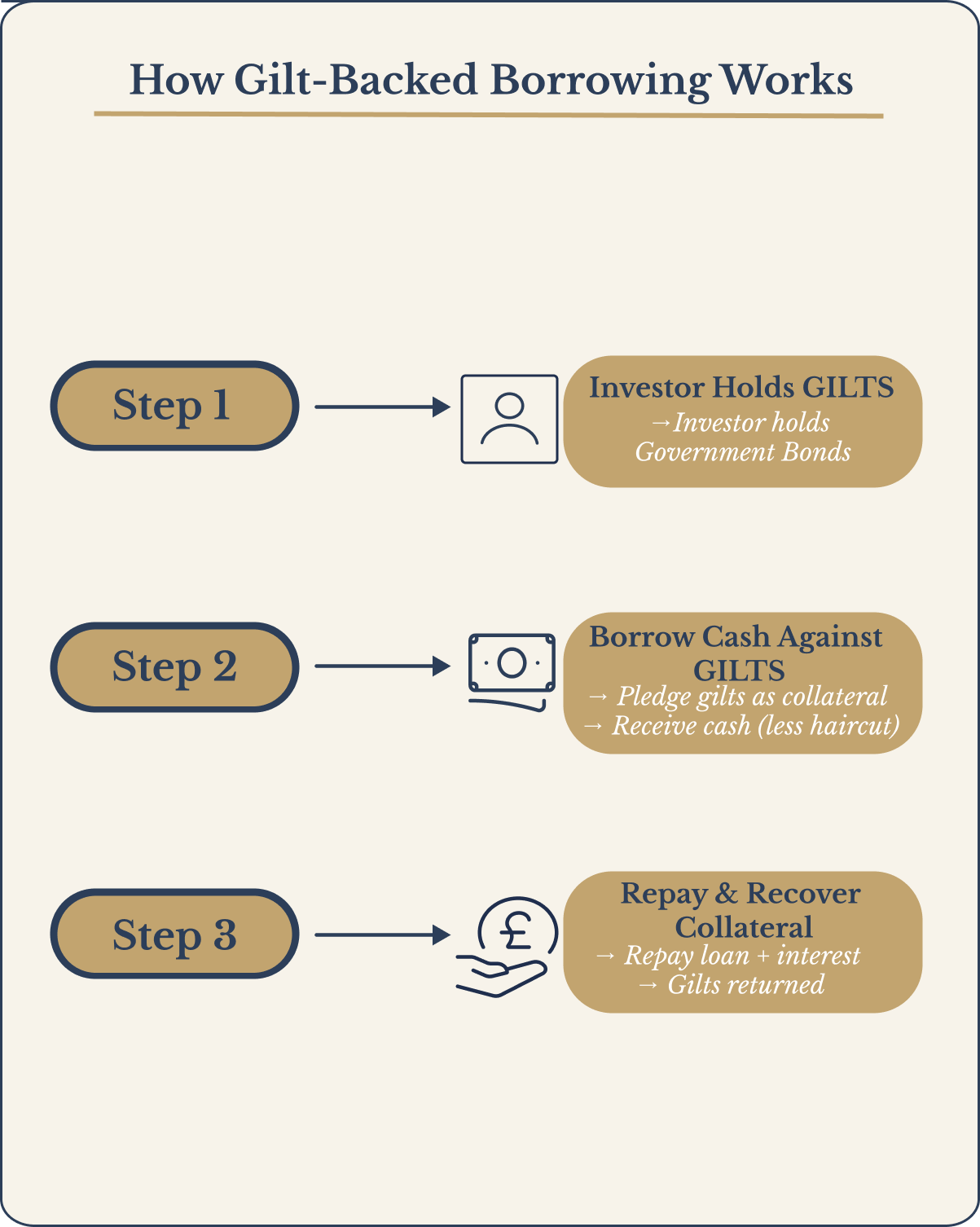

A repo, or repurchase agreement, is a short-term secured financing transaction. One party delivers securities and receives cash, while agreeing to reverse the transaction later at a pre-agreed price. In economic substance, it functions like a collateralised loan.

In the gilt repo market, the securities are typically UK government bonds. That matters because gilts are high-quality collateral and central to the functioning of the UK sovereign debt market. Repo allows market participants to fund gilt positions, obtain short-term liquidity, and circulate collateral through the system.

This is why UK authorities repeatedly frame repo as essential to the functioning of the cash gilt market. Repo supports both the flow of cash and the flow of gilts. If repo markets become impaired, the effects do not remain confined to a narrow funding segment. They can feed directly into gilt market liquidity, price formation, and resilience under stress.

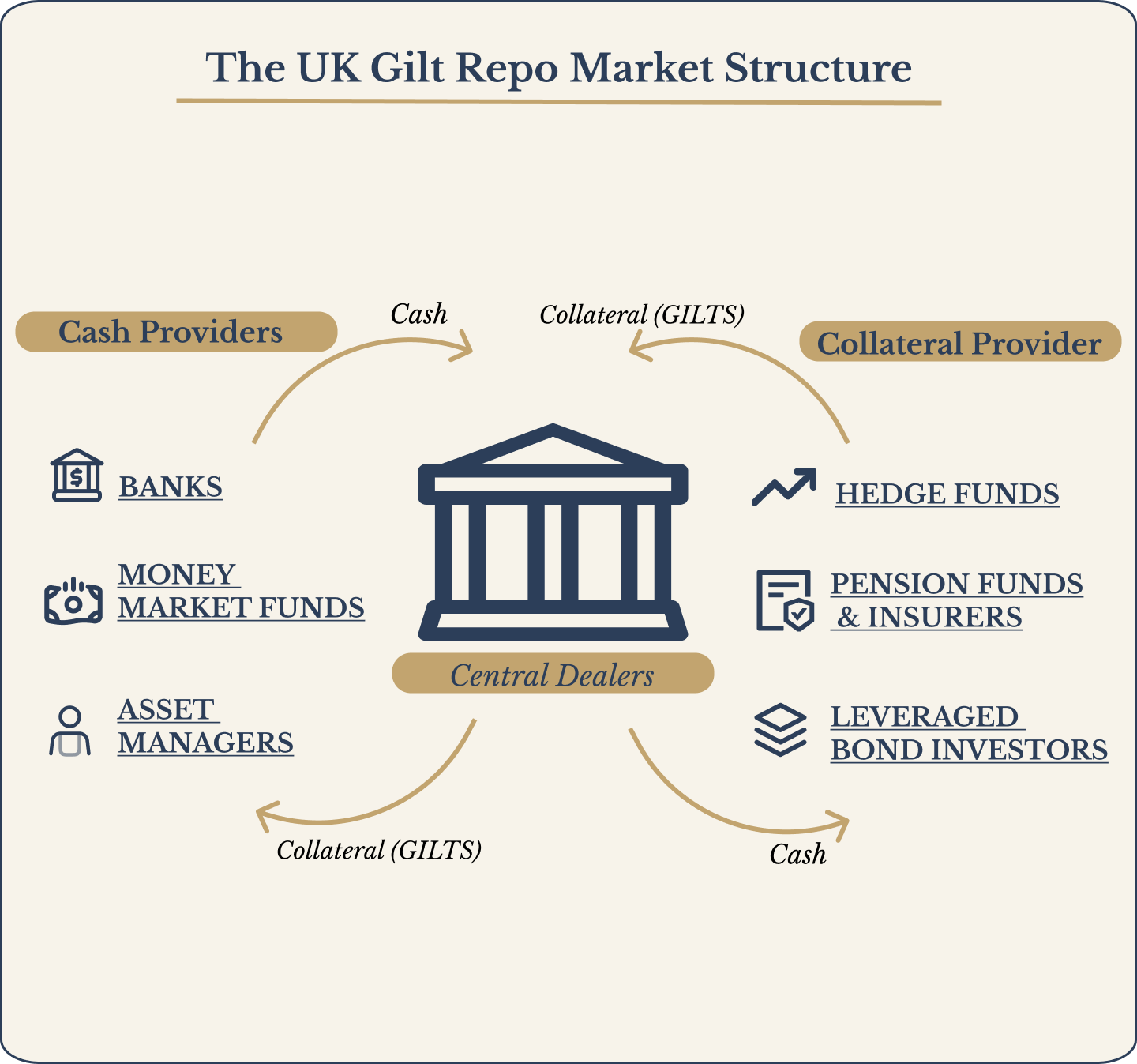

Market structure map: who borrows, who lends, and where risk concentrates

The UK gilt repo market involves a mix of dealers, banks, asset managers, hedge funds, pension-related investors, and other institutional participants. Dealers typically intermediate between cash-rich and collateral-rich parts of the market, helping connect financing demand with available balance sheet and collateral supply.

This intermediation matters because the market is not flat. Risks and dependencies can concentrate in particular participant groups. Authorities have noted the increasing importance of leveraged non-bank participation in gilt markets and the funding channels that support it. Where market actors depend heavily on short-term refinancing, the resilience of repo becomes more important. If that refinancing becomes harder, more expensive, or less available under stress, forced deleveraging can follow.

This is one reason regulators are now focusing not just on whether repo markets function in normal conditions, but on whether they can continue to support gilt market stability when volatility rises and funding conditions tighten.

General collateral vs “specials” and why scarcity matters

Not all repo trades are driven by the same motive. Some are primarily cash-driven, where broadly acceptable collateral is used to obtain funding. Others are security-driven, where a specific gilt is in demand and trades “special.” Public data can be difficult to interpret here, because official repo and stock lending statistics do not always distinguish clearly between general collateral and specials activity. That matters when assessing scarcity, pricing, and signs of stress in collateral availability.

How the UK measures gilt repo activity

One of the most useful credibility tools in this area is the existence of official UK data. The Bank of England publishes further details on gilt repo and stock lending reported to it, including tables on amounts outstanding by maturity and methodological notes on what is being captured.

This matters for two reasons. First, it gives readers a way to anchor discussion in actual reported market structure rather than vague commentary. Second, it helps define terms properly. Reported repo data is typically based on legal agreement structure, and the published breakdowns help clarify what is being measured and how.

For anyone writing seriously about repo, this is a useful discipline: cite the dataset, define the terms, and avoid hand-waving. The UK market has more public official material than many readers assume.

Why resilience is now a policy priority

The current focus on gilt repo resilience is not abstract. It is rooted in recent market history.

UK authorities have repeatedly pointed to March 2020 and September 2022 as stress episodes that exposed vulnerabilities in core market functioning. In March 2020, the “dash for cash” put severe pressure on market liquidity and funding conditions. In September 2022, the LDI crisis showed how margin demands, funding stress, and gilt market dysfunction could interact rapidly.

The policy lesson is clear: authorities want a system that can absorb shocks more effectively without relying on ad hoc intervention every time stress emerges. In that sense, resilience is about whether the market can self-insure and self-stabilise to a greater degree. Repo matters because it sits directly on the boundary between funding liquidity and market liquidity. If repo weakens under stress, gilt market liquidity can weaken with it.

The reform agenda: clearing access, margin procyclicality, and minimum haircuts

The Bank of England’s 2025 discussion paper identifies two broad reform areas.

The first is greater use of central clearing in gilt repo. The second is the potential role of minimum haircuts or margins in non-centrally cleared repo.

The case for greater central clearing is that it may improve resilience by reducing bilateral counterparty risk, improving margin discipline, and increasing the system’s capacity to absorb stress through more structured risk management. But the industry response, as reflected in the 2026 feedback statement, is more nuanced. Respondents recognised potential benefits, including risk management and netting efficiencies, while also highlighting practical barriers, access issues, cost concerns, and questions about the best path forward. In particular, there was concern about whether stronger incentives would work better than hard mandates.

The second reform area is more contentious. The Bank’s discussion paper highlights that haircuts in non-cleared gilt repo can sometimes be very low, or near zero, which can support higher leverage build-up in the system. Minimum haircuts or margin standards are therefore being considered as one possible tool to improve resilience. But the feedback statement also notes market concerns: higher minimums could increase funding costs, affect liquidity provision, and potentially create spillovers into other parts of the market.

This is why the current debate is not simply “more rules versus less rules.” It is about where resilience can be strengthened without unnecessarily damaging market functioning.

What greater central clearing changes operationally

Central clearing changes the structure of counterparty risk. Instead of relying entirely on bilateral exposures, repo participants face a central counterparty, with margining and default management handled within a more formal framework. It can also improve netting efficiency, which matters for balance sheet usage and risk concentration.

Operationally, that means different access models, different margin mechanics, and a different distribution of risk-management responsibilities. The key question for policy is not whether central clearing exists, but how broad and practical access to it can become in the gilt repo market.

Why minimum haircuts are controversial

Minimum haircuts are controversial because they sit at the intersection of resilience and market cost. Policymakers are concerned that near-zero haircuts in non-cleared repo can enable leverage and make stress dynamics worse. Market participants, meanwhile, worry that imposed minimums could raise funding costs, reduce flexibility, and create unintended knock-on effects in liquidity provision.

That tension is likely to remain central to the debate through 2026 and into 2027.

We believe that the next wave of financial innovation will come from companies that combine deep market understanding with scalable technology. Our team is actively working toward building a platform designed to unlock new opportunities within the financial ecosystem.

For those interested in the people and ideas behind this initiative, you can explore the background of our team on our Meet the Team page.

What to watch in 2026–2027

The UK gilt repo agenda is not finished. The Bank has signalled further work through 2026 and indicated that a more comprehensive update, potentially including policy proposals, is expected in early 2027.

The most important areas to watch are likely to include access models for central clearing, how margin and haircut practices behave through the cycle, transparency around non-cleared repo risk, and the broader interaction between market structure, leverage, and resilience.

This matters beyond repo specialists. The gilt repo market is increasingly being treated as part of the UK’s core financial stability architecture. For treasury teams, investors, compliance professionals, infrastructure builders, and policy-focused market participants, this is now a market structure topic worth following closely.

How this relates to Liquida

Traditional repo markets allow institutions to access liquidity against UK gilts, but participation can be operationally demanding, relationship-dependent, and constrained by market structure.

Liquida is building regulated infrastructure that enables institutions to access liquidity against UK gilts in a more modern collateral framework. For anyone thinking about the future of collateral mobility, sterling liquidity, and settlement design, the evolution of the gilt repo market is not separate from that conversation. It is the starting point.

FAQs

What is gilt repo and how is it different from an outright gilt sale?

A gilt repo is a transaction in which gilts are delivered in exchange for cash with an agreement to reverse the trade later. An outright sale transfers the asset with no built-in repurchase leg. In economic terms, repo functions like secured borrowing.

What is the difference between bilateral and centrally cleared repo?

In bilateral repo, counterparties face each other directly and manage credit, margin, and operational processes between themselves. In centrally cleared repo, a central counterparty sits between the parties and manages margining, default handling, and parts of the risk framework.

Why are regulators discussing minimum haircuts in gilt repo?

Because low or near-zero haircuts in non-cleared repo can support leverage build-up and amplify vulnerability under stress. Policymakers are considering whether minimum standards could improve resilience, although market participants have raised concerns about costs and side effects.

Where can I find official UK gilt repo data?

The Bank of England publishes official material on gilt repo and stock lending, including methodological notes and reported data tables. It is one of the best places to start for UK-specific definitions and activity measures.

If you are interested in learning more about our vision, exploring potential collaboration, or discussing investment opportunities, we invite you to connect with our team.

You can learn more about our company on our About Us page, meet the people building the project on the Meet the Team page, or reach out directly through our Contact Us page to start a conversation.

Disclaimer: The content published on this website is provided for informational purposes only and should not be interpreted as financial, investment, or regulatory advice.

Related Posts

Continue Reading

Market Structure & Digital Money

08: The global banking pivot: why tokenised deposits and compliant stablecoins are the emerging mainstream

Major banks are testing stablecoins and tokenised deposits. Here is what that trend means for the UK regulatory direction, settlement infrastructure, and the future of onchain finance.

Continue reading: 08: The global banking pivot: why tokenised deposits and compliant stablecoins are the emerging mainstreamFund Infrastructure & Tax

07: Tokenisation x HMRC

The FCA is progressing fund tokenisation and HMRC is refining DeFi tax approaches. Here is what both directions imply for onchain collateral and compliant markets.

Continue reading: 07: Tokenisation x HMRCSettlement Infrastructure

06: Atomic settlement in central bank money x RTGS synchronisation

The Bank is building RTGS synchronisation to enable atomic settlement in central bank money, including DSS digital securities transactions. Here is what is happening in 2026.

Continue reading: 06: Atomic settlement in central bank money x RTGS synchronisationNewsletter

Get New Research In Your Inbox

When we publish a new article, you will be the first to know.